How to use standard deviation for stock: Guide on volatility

In the simplest terms, the standard deviation for a stock tells you how much its price has strayed from its historical average. A low standard deviation means the stock’s price has been pretty stable and predictable. A high standard deviation, on the other hand, flags a volatile stock with some wild price swings.

What Standard Deviation Reveals About a Stock

Imagine you’re planning a trip. One weather forecast predicts an average of 75°F with a standard deviation of just 2 degrees. Great—you can pack for warm weather with confidence. A second forecast also predicts 75°F but with a standard deviation of 20 degrees. Now what do you pack? You might be facing a chilly 55°F or a scorching 95°F.

That’s exactly how standard deviation works for stocks. It’s the market’s weather report for volatility.

It won't tell you which way the price is headed, but it absolutely tells you how turbulent the journey might be. This single number is a cornerstone of risk assessment, giving you a quick read on a stock's temperament.

Think of a stock's standard deviation as its personality profile. A low number suggests a calm, steady temperament. A high number points to a moody, unpredictable personality prone to dramatic swings.

Gauging a Stock's Risk Level

Getting a handle on this metric is all about matching investments to your own risk tolerance. Are you looking for a slow and steady ride, or are you willing to strap in for a potentially bumpy journey in exchange for higher growth potential?

To put things in perspective, the historical annual standard deviation for a major market index like the S&P 500 typically lands between 15% and 20%. For instance, data from 1992 to 2025 shows the S&P 500 had a compound annual growth rate of 11.02% with a standard deviation of 15.26%. This quantifies how much its returns typically strayed from the average each year. If you want to dig into the numbers, Curvo has some great historical data on S&P 500 returns.

This benchmark is incredibly useful for comparing individual stocks to the broader market. A stock clocking in with a standard deviation of 40% is way more volatile than your average blue-chip, while one at 10% is considerably more stable.

A Quick Guide to Interpretation

To make this really practical, it helps to have a simple framework for what these numbers actually mean for a stock's risk profile.

The table below breaks down what different standard deviation levels generally imply.

Understanding Standard Deviation and Stock Risk

| Standard Deviation Range | Volatility Level | Typical Stock Profile | Investor Suitability |

|---|---|---|---|

| 0-15% | Low | Mature, large-cap companies in stable industries (e.g., utilities, consumer staples). | Conservative investors seeking stability and dividend income. |

| 15-30% | Moderate | Established companies in sectors with some cyclicality (e.g., technology, industrials). | Balanced investors comfortable with average market risk. |

| 30-50% | High | Growth-oriented tech, biotech, or small-cap stocks with less predictable earnings. | Aggressive investors seeking high growth and willing to tolerate large price swings. |

| 50%+ | Very High | Speculative assets like penny stocks, clinical-stage biotech, or crypto-related equities. | Speculators and traders with a very high tolerance for risk. |

Ultimately, there's no "good" or "bad" standard deviation—it's all about what aligns with your strategy and how much risk you're prepared to take on.

Calculating Standard Deviation Step by Step

Knowing that standard deviation measures a stock's volatility is one thing, but actually seeing how the number is calculated is another. Your trading platform will do the heavy lifting for you, but understanding the process gives you the confidence to interpret what you're seeing.

We can break down the math into four simple steps. It turns a scary-looking formula into a logical sequence that anyone can follow.

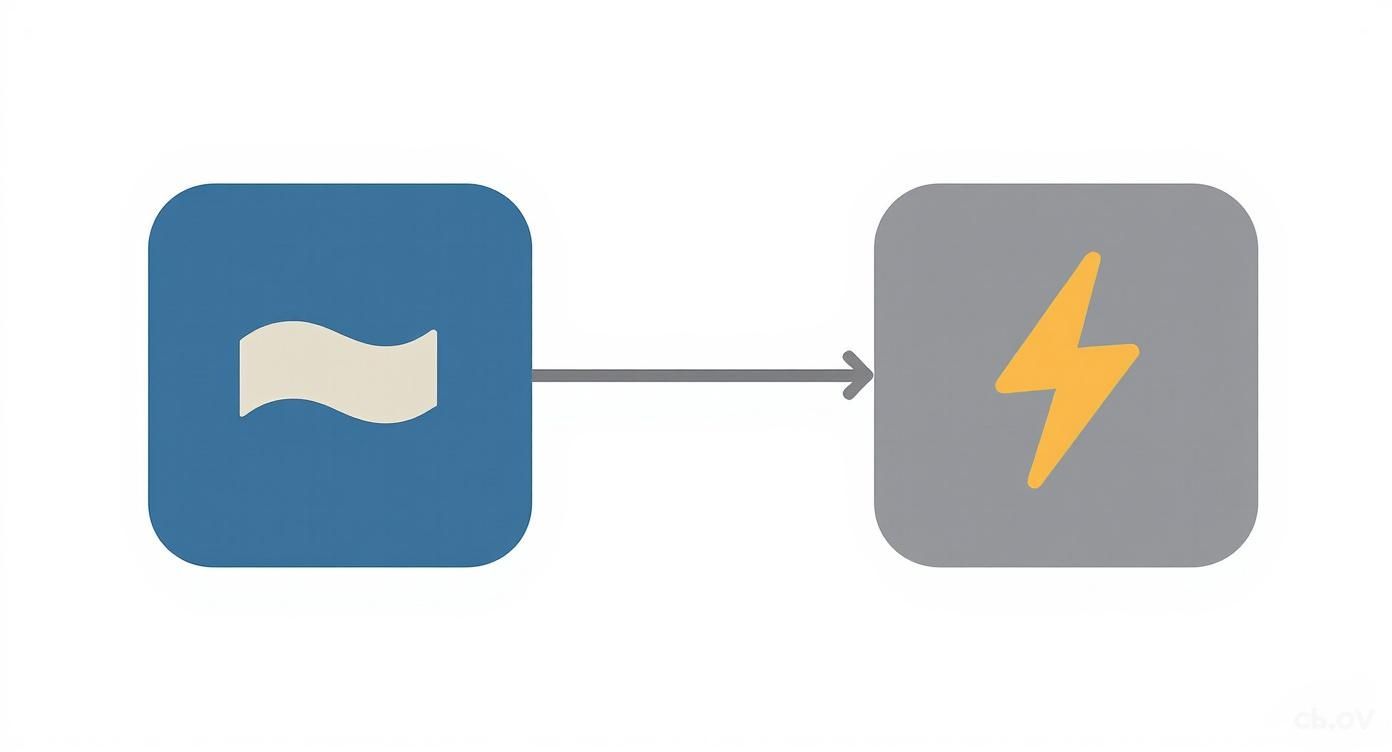

This visual shows the core idea perfectly. A low standard deviation stock is like a calm wave, while a high standard deviation stock is more like a lightning bolt—unpredictable and erratic.

It’s a great mental shortcut: calm wave means lower risk, lightning bolt means higher risk.

The Four Core Steps

You don’t need a Ph.D. in math to get this. Just follow the recipe. Here’s how it works:

-

Calculate the Average Return: Grab your data, like the daily closing prices for the last month. Turn those prices into daily percentage returns. Add up all those returns and divide by the number of days to get the average (or mean) return.

-

Find the Deviations from the Mean: Now, go through each day's return and subtract the average you just calculated. This tells you how much that specific day deviated from the norm. Some days will be positive (better than average), and some will be negative (worse than average).

-

Square and Sum the Deviations: If you just added up all the positive and negative deviations, they'd cancel each other out, which is useless. To fix this, we square each deviation. This makes every number positive. Once they're all squared, add them up to get the "sum of squares."

-

Calculate the Variance and Square Root: Take that sum of squares and divide it by the total number of periods (minus one). This gives you the variance. Finally, take the square root of the variance. Boom. That's your standard deviation for the stock.

A quick but critical note for traders: you'll see formulas that divide by N (the total number of periods) and others that divide by N-1. Since we're always using historical returns as a sample to guess at future volatility, we use the sample formula. That means always dividing by N-1.

A Practical Example

Let’s make this real. Imagine a stock had these wild monthly returns over six months: 8%, 10%, -6%, 15%, -50%, and 24%. That -50% month looks pretty scary, right? Standard deviation will give us a hard number to quantify that risk. You can find more lessons on this kind of investment volatility over at Study.com.

Let’s run the numbers:

-

Step 1: Find the Average Return (8 + 10 - 6 + 15 - 50 + 24) / 6 = 0.167% (basically zero for our purposes)

-

Step 2: Calculate Each Deviation 8 - 0.167 = 7.833 10 - 0.167 = 9.833 -6 - 0.167 = -6.167 15 - 0.167 = 14.833 -50 - 0.167 = -50.167 24 - 0.167 = 23.833

-

Step 3: Square and Sum the Deviations (7.833)² + (9.833)² + (-6.167)² + (14.833)² + (-50.167)² + (23.833)² = 61.35 + 96.69 + 38.03 + 220.02 + 2516.73 + 568.01 = 3500.83

-

Step 4: Find the Variance and Standard Deviation Variance: 3500.83 / (6 - 1) = 700.17 Standard Deviation: √700.17 = 26.46%

The standard deviation for this stock is 26.46% over this six-month window. That’s a high number, and it clearly reflects the massive impact of that one disastrous -50% month. It’s a perfect example of how standard deviation captures a stock's true volatility in a single, powerful figure.

Translating Standard Deviation Into Market Insights

So you’ve calculated a stock’s standard deviation. Now what? That number by itself is pretty useless without some context. The real skill is learning how to translate that raw figure into a story about what the stock might do next.

Think of it as learning to read the language of volatility. One of the best tools for getting fluent fast is the Empirical Rule, also known as the 68-95-99.7 rule. It's a neat statistical guideline that helps you map out a stock's likely range of future returns, assuming its performance follows a somewhat normal pattern.

Understanding The 68-95-99.7 Rule

This rule gives you a practical framework for guessing where a stock's price might end up, all based on its standard deviation. It’s all about probability.

Here’s the simple breakdown:

- About 68% of the time, a stock's annual return will land within one standard deviation of its average.

- About 95% of the time, its return will land within two standard deviations of its average.

- About 99.7% of the time, its return will land within three standard deviations of its average.

Suddenly, you have a probabilistic map of a stock's potential future, which is a much more tangible way to think about risk.

The 68-95-99.7 rule transforms standard deviation from an abstract number into a practical risk management tool. It frames volatility in terms of probabilities, helping you understand the most likely outcomes for your investment.

A Tale Of Two Stocks

Let’s make this real. Imagine we’re looking at two totally different companies: a sleepy, stable utility provider and a high-flying tech startup.

Example 1: The Steady Utility Stock

- Average Annual Return: 8%

- Standard Deviation: 10%

Using our rule of thumb, we can sketch out its likely performance:

- One Standard Deviation (68% Chance): We can expect the return to fall somewhere between -2% (8% - 10%) and +18% (8% + 10%).

- Two Standard Deviations (95% Chance): The return will most likely be between -12% (8% - 20%) and +28% (8% + 20%).

The story here is one of predictability. The outcomes are in a pretty tight, manageable range, which is perfect for a conservative investor.

Example 2: The Volatile Tech Startup

- Average Annual Return: 25%

- Standard Deviation: 40%

Now, let's run the numbers for this one:

- One Standard Deviation (68% Chance): The return could land anywhere from -15% (25% - 40%) all the way up to +65% (25% + 40%).

- Two Standard Deviations (95% Chance): The return could range from a gut-wrenching -55% (25% - 80%) to a mind-blowing +105% (25% + 80%).

This is a completely different beast. The potential for huge gains is there, but so is the risk of catastrophic losses. The standard deviation is screaming "high risk, high reward." For a deeper dive into volatility metrics, it's also worth understanding concepts like Beta in Stocks.

Standard Deviation As A Market Fear Gauge

Standard deviation isn’t just for individual stocks; it’s also a fantastic sentiment indicator for the entire market. When fear and uncertainty take hold, price swings get wilder, and volatility shoots up. A rising standard deviation is the statistical footprint of investor anxiety.

Look back at any major market downturn, like the 2008 financial crisis, and you'll see the standard deviation of broad market returns explode well beyond historical norms. Even within specific sectors, the differences can be stark. For example, the U.S. beverage industry has seen standard deviations ranging from 47.67% for soft drinks to 63.08% for alcoholic beverages, showing just how much risk profiles can diverge.

By keeping an eye on the standard deviation of an index like the S&P 500, you can get a feel for the market's collective mood. A sharp spike is often a clear signal that traders are getting nervous and heading for the sidelines. To better prepare for these shifts, check out our complete guide on what is market volatility. Understanding these dynamics is crucial for navigating turbulent markets.

Using Standard Deviation in Your Trading Strategy

Knowing the theory is one thing, but the real magic happens when you start applying standard deviation directly to your trades. This is where the numbers on a spreadsheet turn into a tangible edge, helping you pinpoint opportunities and, just as importantly, manage your risk.

Instead of just knowing a stock is "wild," you can now put a number on that wildness and build a smarter trading plan around it. Some of the best tools for this are technical indicators with standard deviation baked right into their DNA. They do the heavy lifting for you, turning volatility data into clear visual cues on your charts.

This lets you move past trading on gut feelings and anchor your decisions in what the data is actually telling you.

Pinpointing Opportunities with Bollinger Bands

Bollinger Bands are the classic example of standard deviation at work. Developed by John Bollinger, this indicator plots two bands around a stock's simple moving average (SMA). The key is that these bands aren't static; they are set a certain number of standard deviations away from the middle line—usually two.

Because they're built on standard deviation, the bands breathe with the market. When volatility spikes, the bands get wider. When things quiet down, they tighten up.

This creates a dynamic channel that gives you incredible context for price action:

- Spotting Extremes: When a stock's price hits the upper band, it might be getting overextended or "overbought," potentially due for a pullback. A touch of the lower band can signal the opposite—an "oversold" condition ripe for a bounce.

- Finding the "Squeeze": When the bands contract and get really narrow, it tells you volatility has dried up. This "squeeze" is famous for often preceding a massive price move, acting as a heads-up that a breakout could be just around the corner.

"Bollinger Bands are a fantastic tool because they are dynamic. They don't offer fixed buy or sell signals but instead provide a relative definition of high and low prices, which adapts to changing market conditions."

Technical indicators are a great way to visualize volatility, turning a raw number into an actionable signal on your chart. Several popular tools use standard deviation as their engine.

Trading Indicators Powered by Standard Deviation

| Indicator | How It Uses Standard Deviation | What the Signal Means | Best Used For |

|---|---|---|---|

| Bollinger Bands | Plots bands 2 standard deviations above and below a central moving average. | Prices at the outer bands are considered relatively high or low. The width of the bands indicates volatility. | Identifying overbought/oversold levels and spotting volatility breakouts (the "squeeze"). |

| Keltner Channels | Uses Average True Range (ATR), a volatility measure, to set bands around an exponential moving average. | Similar to Bollinger Bands, but often smoother. Used to identify trend direction and potential reversal points. | Trend-following strategies and gauging the strength of a move. |

| Standard Deviation Channel | Draws parallel lines a set number of standard deviations away from a linear regression trendline. | Shows the expected trading range around the primary trend. Price moving outside the channel can signal a trend change. | Channel trading and identifying when a trend is potentially ending or accelerating. |

While these indicators interpret volatility in slightly different ways, they all share the same goal: to help you understand a stock's price behavior in the context of its own recent history.

Building Smarter Risk Management

Beyond just finding entries, standard deviation is a cornerstone of professional risk management. It allows you to ditch the one-size-fits-all rules and tailor your risk to the unique personality of every stock you trade. Two of the most powerful applications are in position sizing and setting stop-losses.

1. Adjusting Position Size Based on Volatility

It's common sense: a stock that swings 10% a day is far riskier than one that moves 1%. Your position size should reflect that. By using standard deviation, you can keep your dollar risk consistent, even when the stocks are completely different.

Let's say you decide to risk 1% of your capital on any single trade. For a sleepy, low-volatility utility stock, that 1% might let you buy 100 shares. But for a biotech stock with a high standard deviation, that same 1% risk budget might mean you can only buy 30 shares. This simple calculation prevents one wild stock from blowing up your account.

2. Setting More Effective Stop-Loss Orders

Ever set a stop-loss only to watch the price dip down, tag you out, and then immediately reverse in your favor? It's incredibly frustrating, and it often happens because the stop was too tight for the stock's normal behavior.

Standard deviation helps you set stops that respect a stock's natural rhythm. Instead of a generic 5% stop, you could place it 1.5 or 2 standard deviations below your entry. This data-driven approach, sometimes called a volatility stop, gives your trade the room it needs to fluctuate without kicking you out on random noise. You're aligning your risk with how the stock actually trades.

Tools to Automate Your Volatility Analysis

Let's be real: manually calculating standard deviation for a list of stocks every single day is a non-starter for any serious trader. If you truly want to weave volatility analysis into your strategy, you need tools that do the heavy lifting for you—instantly and reliably. The good news is, you probably already have access to everything you need to get this process automated.

Moving from manual crunching to automated analysis frees you up to focus on what actually matters: interpreting the data and making smart trading decisions. Whether you're comfortable in a spreadsheet or prefer a dedicated platform, the goal is to make the numbers work for you, not the other way around.

This is how you stop being a number-cruncher and start building strategies based on real-time volatility insights.

Quick Calculations in Excel and Python

For quick, one-off analyses, spreadsheets and simple scripts are your best friends. They let you pull in historical price data and compute volatility in seconds, making it easy to compare a few different stocks or do a deep dive on a single name.

Using Microsoft Excel

Excel is a go-to for many traders because it's just so simple. If you have a column of daily or weekly returns—say, in cells A2:A22 for a 20-day period—calculating the sample standard deviation is a piece of cake.

- Formula:

=STDEV.S(A2:A22) - How it Works: The

STDEV.Sfunction is built specifically for sample data, which is exactly what historical stock returns represent. Just feed it the range of your returns, and Excel spits out the standard deviation for that period instantly.

Using Python with Pandas If you're more comfortable with code, Python offers a far more powerful and scalable solution. The Pandas library, in particular, is perfect for handling time-series data like stock prices.

import pandas as pd

Assume 'returns' is a Pandas Series of daily stock returns

For example: returns = df['Close'].pct_change().dropna()

Calculate the 20-day rolling standard deviation

rolling_std_dev = returns.rolling(window=20).std()

To get the latest value

latest_volatility = rolling_std_dev.iloc[-1]

print(f"The 20-day standard deviation is: {latest_volatility:.4f}") This little snippet calculates a rolling standard deviation. This is infinitely more useful for active trading because it gives you a dynamic, up-to-date measure of volatility, not just a static historical figure. Many traders lean on different kinds of reliable financial software to automate their analysis and keep data manageable.

Setting Up Automated Scans and Alerts

While doing a quick calculation is handy, the real magic happens when you set up automated systems to watch the market for you. This is where dedicated stock scanners like ChartsWatcher enter the picture, letting you shift from analyzing the past to finding future opportunities as they happen.

The point of automation isn’t just to save time. It's to systematically find trading setups that match your specific volatility rules. This turns a reactive chore into a proactive, opportunity-finding machine.

Instead of looking at one stock at a time, you can scan the entire market for very specific volatility conditions. For example, you could build a scan that finds stocks meeting criteria like these:

- Low Volatility Squeeze: Pinpoint stocks where the 20-day standard deviation has dropped to a 6-month low. This often signals a Bollinger Band squeeze right before a big breakout.

- Volatility Expansion: Get an alert for any stock whose standard deviation suddenly spikes more than 50% above its 3-month average, which could mean a powerful new trend is kicking off.

- High-Momentum, Stable Stocks: Filter for stocks in a strong uptrend but with a standard deviation below 25%. This helps you find growth stocks that aren't excessively wild.

By combining different indicators, you can create a highly targeted watchlist of stocks that perfectly fit your trading style. Choosing the right platform is key; if you need more guidance, this guide to stock market analysis software is a great resource. Ultimately, automation gives you the power to monitor thousands of stocks at once, ensuring you never miss an opportunity that aligns with your strategy.

Knowing the Limits of Standard Deviation

While standard deviation is a go-to risk metric for stocks, it's critical to understand that it doesn't tell you the whole story. Relying on it exclusively is a bit like driving a car using only the speedometer—you know how fast you're going, but you’re missing the bigger picture of the road ahead. Its greatest strength is its simplicity, but that simplicity also creates some serious blind spots.

The biggest issue is that standard deviation assumes stock returns follow a "normal distribution," which looks like a perfect, symmetrical bell curve on a chart. But in the real world, markets are anything but normal. They're messy and prone to sudden, extreme events—think market crashes or explosive rallies—that the neat and tidy bell curve model treats as nearly impossible.

The Problem with Black Swan Events

These unexpected moments, often called "black swan" events, fall far outside the predictable ranges of one or two standard deviations. The 2008 financial crisis and the 2020 pandemic crash are perfect examples. Standard deviation is great at measuring the everyday bumps in the road, but it completely fails to account for these catastrophic tail risks that can absolutely devastate a portfolio.

Another major flaw is how it treats all price swings equally.

Standard deviation is blind to the difference between good and bad volatility. A stock that surges 20% above its average and one that plummets 20% below are both treated as equally "risky" by the formula. As investors, we know that’s not true—the pain of a big loss is felt far more than the joy of an equivalent gain.

This symmetrical view of risk just doesn't line up with the real-world goals of most traders, which is primarily to protect capital from those nasty downside moves.

Adding Nuance with Other Risk Metrics

To get a more refined view of risk, sophisticated traders and investors pair standard deviation with other metrics. These tools help you see not just how volatile a stock is, but how effectively it has rewarded you for taking on that volatility in the first place.

Two of the most popular complementary metrics are:

- Sharpe Ratio: This metric measures a stock's return after subtracting the risk-free rate, all divided by its standard deviation. It neatly answers the question: "Am I getting enough return for the amount of volatility I'm enduring?"

- Sortino Ratio: This is a clever twist on the Sharpe Ratio. Instead of using the total standard deviation, it only considers downside deviation—the volatility of negative returns. It specifically focuses on the "bad" volatility that actually keeps investors up at night, providing a much more intuitive measure of downside risk.

By using these tools alongside standard deviation, you can start building a more resilient and intelligent investment strategy that goes beyond simple volatility to understand true risk-adjusted performance.

Got Questions? We've Got Answers

Once you start digging into standard deviation, a few practical questions always pop up. Let's tackle the most common ones so you can start using this metric with more confidence.

What Is a Good Standard Deviation for a Stock?

This is the million-dollar question, but the answer is: there’s no magic number. A "good" standard deviation is completely personal and depends entirely on your own risk tolerance and what you’re trying to achieve.

A conservative investor who prizes capital preservation and steady dividend checks would probably find a low standard deviation (say, under 15%) very attractive. It points to stability and a smoother ride.

On the flip side, an aggressive growth investor hunting for explosive returns might be totally comfortable with a stock that has a standard deviation of 30% or more. The "right" number is the one that fits your strategy and lets you sleep soundly at night.

How Often Should I Check a Stock's Standard Deviation?

The best frequency really comes down to your trading style. You want your analysis timeline to match your holding period.

- For Long-Term Investors: Looking at standard deviation quarterly or even annually is usually fine. You're focused on the big picture, so you can ignore the short-term noise.

- For Active Traders: You need to monitor volatility much more closely. A rolling 20-day standard deviation is a popular choice because it gives you a real-time feel for the stock's recent behavior, which is critical for timing entries and exits.

Can Standard Deviation Predict a Market Crash?

In a word, no. Standard deviation is a reactive metric, not a predictive one. Think of it less like a crystal ball and more like a speedometer for the market. It tells you how wild the ride is right now, not where it's headed.

That said, it can be a powerful warning sign.

When you see the standard deviation of a major index like the S&P 500 start to spike, it’s a clear signal that fear and uncertainty are creeping in. While it doesn’t guarantee a crash is coming, it absolutely flags the kind of nervous environment that often precedes a major downturn, telling smart investors it's time to be more cautious.

Ultimately, standard deviation is a fantastic tool for taking the market's temperature in the present moment.

Stop relying on guesswork and start building data-driven trading strategies. ChartsWatcher provides the advanced scanning and backtesting tools you need to find opportunities based on volatility, momentum, and more. Take control of your analysis at https://chartswatcher.com.